Like many, recent conversations have involved the advancements of Artificial Intelligence (more generally) and its impact on financial advice (more specifically). Personally, I have looked for ways in which I can benefit my clients and improve my practice ‘lifestyle’ without losing focus by chasing the latest fad.

I am excited about the recent developments in Artificial Intelligence and its rapidly increasing impact on our world. And, I am not just saying that to curry favour with my future computer overlords! It is inspiring to see the innovation, productivity increases, and pure excitement that Artificial Intelligence apps are creating. Beyond the ‘wow factor’ of ChatGPT and DALL-E though, there are broader implications of the types and potential risks of AI to consider. Even the current debate on how to best regulate these services causes us to ask ourselves questions about the type of society we wish to have in the future.

Advancement brings Disruption

Inevitably, indeed almost by definition, these advancements will bring significant disruption. If not, what’s the point? But the disruption will flow into a restructuring of our economy and, I believe, make a profound impact on our future workforce. Author and Physicist Max Tegmark explores many of the possible scenarios and issues in his excellent book Life 3.0. These range from a world of leisure and secure income to the complete annihilation of humanity as consciousness evolves to a non-organic form and humans lose their utility!

On a more immediate scale, it’s tempting for financial advisers to reject the notion that their expertise could be threatened by AI – or more particularly, Large Language Models such as ChatGPT. After all, our work is built on the trust we develop over a long period of time, and on our technical expertise. Others posit a value proposition of superior investment performance. But complacency is naive and solipsistic.

I recall a friend of mine back in the 80s, who had completed an apprenticeship as a Typesetter. His entire vocation disappeared overnight with the introduction of software to replace the physical laying out of metal type in blocks for printing. My friend was left in his late 20s with no other employable skills. Try talking to him about the wonders of computer technology!

Many financial advisers are in denial about the impact that AI and technology will have on our profession. Others simply hope that they will be spared and manifest this by continuing to offer more of the same, relying on market inertia to guarantee their success (at least until they retire or move on for their own reasons). To me, this is naive at best, and pusillanimous at worst. AI will result in profound changes to how we advise clients. But it offers staggering possibilities to improve as well. These need to be understood and faced.

So what are the most significant promises and the greatest threats that financial advisers (and by extension, our clients) face from AI? Are there any aspects of our work that are safe from AI challenges?

As I see it, anything data-related or driven is immediately up for grabs. AI is simply built differently from humans and designed to process data in ways that are different and more efficient than our brains.

The Promise of Artificial Intelligence for Financial Advisers

The promise of AI is that it can relieve our profession of the lowest-value but necessary work and allow advisers to focus on what adds the most value to the client relationship – or more precisely, on what the clients that we seek to serve value the most.

An area of significant promise is portfolio construction and management. Portfolio construction – despite the protestations of many – is in my opinion as much of an art as a science at a human level. No one person or even firm can consider the entirety of the investment universe, and construct a portfolio that still also meets regulatory hurdles let alone the needs of a client as it relates to their tolerance for risk, access to capital and cash flow requirements. This is not a criticism, as the abundance of options means that the achievement of an investor’s goals is not hindered by this fact.

But portfolios are often viewed as photographs, whereas in reality, they are more akin to motion pictures. Investments go up and down in value, markets change, and new products and securities are being introduced all the time. In other words, there is a staggering volume of data to be considered, selected, assessed and then applied to an individual’s portfolio.

It’s in this area that I see AI having a tremendous benefit to investors because it promises to be able to continuously market data with an individual’s preferences and objectives to optimally maximise a portfolio to be fit for purpose. Imagine a system that had delegated authority to apply qualitative screens (e.g. regulatory approval, liquidity, currency) and act automatically to either buy, sell or rebalance based on both mathematical and statistical analysis of a portfolio as well as the subjective preferences of the individual client. A system that could concurrently allocate assets appropriately for the time horizon of the portfolio whilst properly timing trades to market conditions on that day. And to achieve all this within the context of a particular client’s cash flow requirements and taxation profile?

It is dangerous for financial advisers to consider their experience, expertise or even technical ability as some sort of moat guaranteeing a sinecure.

Investment advisers may reel with horror at this suggestion that AI steals their alpha (though conceivably it could create other arbitrage opportunities – but that’s a discussion for another day) but as an independent financial adviser I would welcome such a time-saving service as a way to ensure that investment choices were effectively implemented and managed.

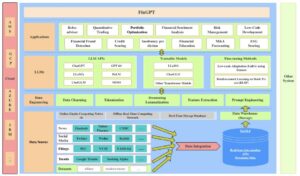

But such a Financial AI service – ‘FinGPT’ faces some very practical challenges, as identified in a recent paper outlining a design for a FinGPT Large Language Model. Simply accessing the data – both historical and current – in a non-proprietary and consistent format poses a significant practical challenge. How do you extract and equate, for example, Earnings per share across stocks and jurisdictions? What about comparing dividend yields on Australian stocks between resident and non-resident investors, or the effect of depreciation rates on REITs? The devil, as always, is in the details.

Figure 1: FinGPT Framework (Yang, Liu, Wang 2023)

These will be overcome, but what about issues of liability and the fulfilment of KYC and AML requirements? I’ve yet to see a licensing regime that will accredit computer code, nor a jurisdiction that will allow a client to take action against a software program. Liability remains with a legal entity, and prudent advisers will want to understand and approve any recommendations – effectively advice – provided by a FinGPT. So does this negate or materially reduce any productivity benefits this might bring?

An Adviser’s Competitive Edge

There are many benefits to engaging a financial adviser (I would say that, wouldn’t I?) In my experience though, the one that gets either overlooked or taken for granted is one of the most valuable. Financial advisers precipitate and enhance the agency of their clients. That is, they make sure important stuff gets done. It’s quite true that any plan is usually better than no plan, and working with an adviser – a human adviser – means that decisions get made, actions are taken, follow-ups are made: shit gets done.

So often when I first meet with even the most experienced clients, they know roughly what needs to be done. Often they even know where to start, and how to implement it. However, they are looking for the encouragement and reassurance that an experienced independent adviser can provide.

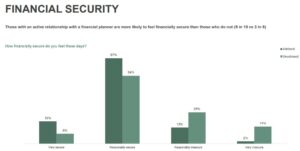

Figure 2: Sense of Financial Security (FAAA 2022)

The manifestation of this call to action is reflected in qualitative research on the value of financial advice. Both the Financial Advice Association of Australia and the Financial Planning Association of Canada have conducted research shopping the reported improvement in the overall wellbeing of advised versus non-advised persons. These are second-order effects but are, I believe, highly correlated with a strong sense of agency at the level of the individual investor.

This sense of agency, of empowerment, is an advantage that I believe financial advisers will always have over non-human advice providers like AI or robo-advice. It goes beyond simple email reminders or phone alerts. It is the nuanced understanding of client psychology that even the best Turing machine will struggle to replicate, because the financial adviser often makes the first call, rather than waiting for someone to respond.

How does this play out?

My sense is that AI will increasingly support financial advisers through their use in performing tasks that are technically complex and data-driven, such as portfolio construction and research. Gradually, this will evolve to include true robo-advice that is focussed on specific goals or particular products (e.g. superannuation in Australia) and in only one jurisdiction.

Of course, as data collection and reporting move to fully standard and open-source, the depth and quality of financial advice produced by AI will continue to improve.

Daniel Susskind (co-author of the prescient and excellent book Future of the Professions) hit the nail on the head recently when he wrote “To claim clients want expert, trusted advisers is to confuse process and outcome. Patients do not want doctors, they want good health. Clients do not want litigators, they want to avoid pitfalls in the first place. People want trustworthy solutions, whether they rely on flesh-and-blood professionals or AI.”

It’s easy to forget how quickly and silently societal morés change over time, without us being aware. Remember when mobile phones became truly mobile, and (in Australia at least) those who conducted a call whilst walking down the street were seen as ostentatious poseurs. Now we can’t switch the damn things off.

So I tend to agree with Susskind. It is dangerous for financial advisers to consider their experience, expertise or even technical ability as some sort of moat guaranteeing a sinecure. You ignore the market and take your clients for granted, at your peril.

But while I am in a nostalgic mode, I also remember a truism from my early days as an advisor: Insurance is not bought, it has to be sold. Equally, the best financial plan means little if action is not taken, or steps are not implemented accurately and effectively. My AI apps are fantastic at responding to my queries and (at least for now) don’t have the ability to tap me on the shoulder and inspire me to take action.

I’d love to hear your views – contact me here to start a conversation.

Geek Corner

I would like to give credit to DALL.E 2 for generating the header image on this post!