Where is the Value in Financial Advice?

It’s axiomatic that every single client I have ever seen is seeking to improve their situation. The challenge lies in identifying exactly what improvement is required and how this can be measured.

Financial Planners can conduct a range of services for their clients. Most are orthodox: cash flow planning, asset allocation and investment recommendations, estate planning. Some less so: in my career I have helped in mergers & acquisitions, lawsuits and even a few death-bed visitations. All of these services are demonstrably valued to at least the extent that our clients retain our services. But is there a better way to determine value?

A recurring challenge for both financial advisers and their clients has been, how do you quantify the value that is created? Is it simply looking at the increase in one’s Bank Balance? An army of asset managers will answer with a resounding YES. Yet it is simplistic to assume a linear relationship between wealth and satisfaction.

Never ignore the possibility that sometimes the best advice is to spend money, especially in later life. Or should we seek the highest percentage rate of return on a portfolio? Perhaps, except that in many cases we don’t look for the highest return, we look for the best risk-adjusted return.

The overarching purpose of quality financial advice is to improve financial wellbeing. Personally, I believe that people and families that enjoy high levels of financial wellbeing live happier, healthier and more prosperous lives. This in turn impacts their broader community, and it is not a stretch to say that this made, at least in their corner, the world a better place.

What is Wellbeing?

Wellbeing is one of those concepts that most feel they understand intuitively. To describe and define it is another thing altogether. Researchers themselves argue over whether measuring wellbeing is something that can be assessed objectively or if it should remain a subjective assessment.

There have been efforts to define and measure wellbeing objectively, although these are not without challenges. Wellbeing is not an easily measured or counted number like a nation’s economic output. As Robert Kennedy observed: ‘the gross national product does not allow for the health of our children, the quality of their education or the joy of their play. It does not include the beauty of our poetry or the strength of our marriages, the intelligence of our public debate or the integrity of our public officials. It measures neither our wit nor our courage, neither our wisdom nor our learning, neither our compassion nor our devotion to our country, it measures everything in short, except that which makes life worthwhile’.

This does not mean that wellbeing cannot be measured. But first, it should be understood and defined.

Researchers have identified three broad types of wellbeing:

Life Evaluation:

Life evaluation refers to people’s thoughts about the quality or goodness of their lives, their overall life satisfaction, or sometimes how happy they are generally with their lives.

Hedonic Wellbeing:

Hedonic wellbeing is sometimes defined as ‘experienced’ wellbeing. It is centred on positive emotions, pleasure and satisfaction. Feelings such as sadness, anger, illness and pain diminish this perception.

Eudemonic Wellbeing:

Eudemonic wellbeing relates to a sense of purpose and meaning in life. It is a sense of wellbeing derived from living according to one’s values, being true to oneself, reaching your full potential and developing personally.

As can be seen, there may be many circumstances where these three types of wellbeing do not correlate within an individual. Anyone who has gone on a fitness regime can relate to sacrificing Hedonic wellbeing for increased Eudemonic wellbeing as the pain of a diet or exercise is (hopefully more than) compensated with the feeling of being true to our personal potential.

To better understand and measure these interactions, a more granular distinction in wellbeing is required. The Gallup organisation has developed a Global Wellbeing index, which is designed to measure the behavioural economics of gross national wellbeing. To do this, they measure overall wellbeing in five components:

Purpose (or Career) Wellbeing:

Liking what you do each day and being motivated to achieve your goals.

Social Wellbeing:

Having strong relationships and love in your life

Financial Wellbeing:

Managing your economic life to reduce stress and increase security.

Community Wellbeing:

Liking where you live, feeling safe and taking pride in your community.

Physical Wellbeing:

Having good health and enough energy to get things done daily.

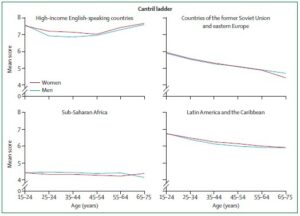

Interestingly, Gallup’s data shows a U-shaped relation between wellbeing and age in high-income, English-speaking countries. Wellbeing begins to decline in the mid-40s and only starts increasing again in the early to mid-50s. There is scientific evidence for the mid-life crisis!

Figure 1: Life evaluation and age in four regions (Steptoe et al, 2014)

There is scientific evidence for the mid-life crisis!

There is a growing consensus among academic experts and policymakers that, of the five components, it is financial wellbeing that is the ultimate measure of success for individuals’ overall wellbeing. A society that faces financial constraints also faces profound consequences for its overall welfare. The state of living in financial instability, in poverty, or having financial problems has a detrimental impact on single individuals, their families and society collectively. The lack of financial wellbeing can lead individuals to live precariously, affects their economic mobility and may transform a small financial problem into an ongoing financial constraint.

Very importantly, financial vulnerability and low financial wellbeing seriously affects and distresses a worker’s productivity.

This research is supported by my experience with assisting clients in improving their financial wellbeing over decades. I’ve seen first-hand the difference being financial organised makes in a person’s self-esteem and peace of mind. This assuredness can and does radiate out into other areas of their lives.

What is Financial Wellbeing?

Like wellbeing generally, financial wellbeing can be challenging to define. It is not simply being financially affluent: we’ve all known people who are wealthy yet unhappy, or poor yet without a care in the world. Equally, simply understanding or knowing a lot about money, taxes, share markets or property does not guarantee financial wellbeing either.

Research shows us that subjective knowledge and how we behave with money has a stronger correlation with financial wellbeing than education alone. This is not to say that improved financial literacy is not important. Understanding how money and our financial system works is an essential skill to master in order to participate in our modern society. Yet, it is not enough to simply promote financial literacy – we must also consider encouraging confidence and motivation to act in order to increase financial wellbeing.

The Institute for Financial Wellbeing (IFW) in the UK describes financial wellbeing as ‘how money can be used to increase our happiness.’ As noted above, the other areas of wellbeing are very dependent upon financial wellbeing for their function. Therefore, it is about how we use our money to support other areas of wellbeing.

The IFW has taken this further and identified five factors that contribute to financial wellbeing. At Kenwell, we have integrated these elements into our financial advice programs, whether these are provided on an individual or group basis, face-to-face or via our online platforms.

These five elements are:

Clear, Identifiable Objectives:

One of the greatest contributing factors to stress in life (regardless of the subject) is uncertainty. Identifying and quantifying financial objectives is the essential first step towards achieving these. Simply deciding what you wish to achieve with your money is empowering.

Control over Daily Finances:

Prudent financial management is a critical element for financial wellbeing. This means understanding where your money comes from, and where it goes. Without this knowledge, priorities cannot be consciously established, and wellbeing (and wealth) remains hostage to factors outside of your control.

Ability to withstand Financial Shocks:

My experience teaches me that the only certainty in financial markets is uncertainty, and this is true for even the best-laid plans. Even in calm times, preparation for unexpected events needs to be put into place. Whilst uncertainty and shocks cannot be avoided, their impact can be managed and planned for.

Financial Options:

When you need money, you need a smart place to get some from. This could be savings, or credit, or simply varying your spending habits. Having different options on how and where to access your financial resources is an important contributor to financial wellbeing. Equally, understanding what trade-offs may be necessary to take with each of the options is an empowering experience.

Clarity and Security for our Family and Loved Ones:

Although an individual measure, financial wellbeing is influenced by our interactions with family and friends. Money itself depends on the framework of our societies’ laws and institutions, and its subjective value on our stage of life. Assuring those close to you of your values, intents and instructions is a very real part of increasing financial wellbeing, regardless of what stage you are at in life’s journey.

Having now arrived at a conceptual understanding of wellbeing, and a definition of financial wellbeing, how can this be applied for your benefit?

In other words, what practical steps can be taken to increase your own financial wellbeing and how do you measure this?

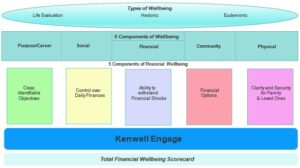

Figure 2: Interrelationships of Financial Wellbeing, Kenwell Engage with overall wellbeing.

The good news is that, with the appropriate attention, enhancing one’s financial wellbeing is entirely within an individual’s control.

Why is Financial Wellbeing important?

We live in a society that is increasingly interconnected through digital communication, and transacting using electronic currency via either debit or credit cards. Current trends suggest that it will not be long before people not only completely manage their financial lives virtually, but they will have to also choose which currencies (fiat or crypto) to use. Money, whilst fungible, is almost completely virtual and intangible. Good financial literacy is obviously important for an individual’s personal success. But, as we have explained above, financial wellbeing goes beyond a simple intellectual understanding of financial concepts. Financial wellbeing involves a sense of control and preparedness, and an experiential grasp of money usage.

The lack of financial wellbeing manifests itself in some concerning societal statistics. In the UK in 2018, 47% of workers experienced some degree of financial difficulties and over half (51.1%) reported financial worries. Employees who have these financial difficulties can be up to half as productive as those without.

Similarly, more recent research in the UK also shows that 55% of average income earners and 1 in 3 high income earners worry about money; 45% don’t feel confident in managing their quotidian finances.

We fully expect similar situations in developed economies, as they face similar circumstances and trends. Arguably, the need to address the lack of financial wellbeing has never been greater if families and individuals are to achieve a better quality of life.

Measuring Financial Wellbeing

Of course, defining and understanding financial wellbeing is one thing, but how do we measure this improvement? Without a robust methodology, the risk is that any improvement in financial wellbeing becomes anecdotal, ephemeral or simply conjectural.

An intuitive response to anything to do with money is to look to financial measures as a yardstick. What improvements have there been in cashflow? Has the person’s savings or income increased? Have they prepared and kept to their budget? These are all important matters but are only loosely correlated to financial wellbeing.

There is plenty of research showing that increased wealth does not necessarily positively correlate to financial wellbeing. We all know the stories of wealthy but unhappy people. Similarly, increasing income has a diminishing positive impact on financial wellbeing – that is, above certain levels more income makes virtually no difference. So, it is not simply a matter of becoming wealthier or earning more income.

As financial advisers, we understand that sometimes, especially in later life, the best advice is to actually spend money! Or, in times of market volatility, the best action is no action, allowing the market to recognise the intrinsic value of assets held.

For these reasons, my colleagues at Verse Wealth developed a Financial Wellbeing Scorecard. This simple self-assessment allows for a measure of financial wellbeing and places this within the context of the person’s overall wellbeing. It provides a reliable self-assessment that can be compared over time.

The Financial Wellbeing Scorecard is a basis by which a financial adviser can measure the value of the services provided over time through financial advice and consulting services.

What’s Next?

Positive and high wellbeing is an important and valuable contributor to one’s overall quality of life and happiness. Understanding the five areas that contribute to this and living in a fashion designed to enhance them is a way of living that is to be recommended.

Financial wellbeing itself is shown to be the critical component that can positively influence the other four elements. The good news is that, with the appropriate attention, enhancing one’s financial wellbeing is entirely within an individual’s control. As a financial adviser, it is this criterion, rather than the bank balance, around which I base my personal advice.

By engaging with this perspective, specific investment and structural recommendations can be made with the aim of improving financial wellbeing. And, by measuring this over time, we have a relevant and objective self-assessment to measure the value that this advice brings.

Want to know more? Contact me today to start the discussion!

References

Abrantes-Braga, Farah Diba M.A, and Tania Veludo-de-Oliveira. “Development and Validation of Financial Well-Being Related Scales.” International journal of bank marketing 37.4 (2019): 1025–1040

Aegon ‘Our insight into the nation’s financial wellbeing’ 2021

Ali, Shahzad, and Nighat Talha. “During COVID-19, Impact of Subjective and Objective Financial Knowledge and Economic Insecurity on Financial Management Behavior: Mediating Role of Financial Wellbeing.” Journal of public affairs (2021): e2789–e2789.

Berstein, Shai, McQuade, Timothy, and Townsend, Richard “Do Household Wealth Shocks Affect Productivity? Evidence from Innovative Workers During the Great Recession.” The Journal of finance (New York) 76.1 (2021): 57–111.

CIPD/You Gov COVID Working Lives Survey, June 2020 https://www.cipd.co.uk/knowledge/work/trends/goodwork/covid-impact#gref

Cooper, Cary L., and Ian. Hesketh. Managing Health and Wellbeing in the Public Sector: A Guide to Best Practice. 1st ed. Milton: Taylor & Francis Group, 2017.

Gallup Inc, “Well-being: What you need to Thrive” 2010 https://news.gallup.com/businessjournal/127643/wellbeing-need-thrive.aspx

Kirkwood, Thomas and Cooper Cary. Wellbeing: A Complete Reference Guide. (Wellbeing in Later Life). IV. Wiley-Blackwell, 2014.

Iacus, Stefano M., and Giuseppe. Porro. Subjective Well-Being and social media. Milton: CRC Press LLC, 2021

Money and Pensions Service Financial Wellbeing Survey 2021 https://www.maps.org.uk/2022/03/28/financial-wellbeing-survey-2021/

O’Connor, Genevieve, and Sertan Kabadayi, Exploring Financial Wellbeing. Emerald Publishing Limited, 2019.

Personal Group ‘Financial Wellbeing Report for Employers’, 2021

Riitsalu, Leonore, and Rein Murakas. “Subjective Financial Knowledge, Prudent Behaviour and Income: The Predictors of Financial Well-Being in Estonia.” International journal of bank marketing 37.4 (2019): 934–950.

Secondsight ‘The Personal financial wellbeing assessment’ 2021

Steptoe, Andrew, Angus Deaton, and Arthur A Stone. “Subjective Wellbeing, Health, and Ageing.” The Lancet (British edition) 385.9968 (2015): 640–648.

Vernon, Mark. Wellbeing. Stocksfield: Acumen, 2010.