Central Bank Digital Currencies (CBDCs) simultaneously represent one of the most exhilarating and menacing investment developments for international investors. They offer the prospect of reducing transactional friction and lending jurisdictional credibility to cryptocurrencies. However, they also pose grave threats to individual privacy, sovereignty, and orthodox capital investments.

The Relevance of CBDCs for International Investors

The quest for understanding the relevance of CBDCs to international investors invites a deeper exploration into the threats and opportunities they present. If these digital currencies proceed on their trajectory, they could significantly impact the established financial system.

In June, the European Union issued a press release that intriguingly covered the spectrum of currency manifestations. It outlined proposals to provide legislative certainty for Central Bank Digital Currencies (CBDC) as well as guarantee the ability for EU citizens to continue to use cash in transactions.

This caught my eye because, in many circles, CBDCs are seen as antithetical to the use of “the folding stuff”. A CBDC, in the simplest of terms, is electronic currency, issued by a Sovereign Nation using a private blockchain, carrying equal weight and value as a unit of their traditional fiat currency. Arguably it is the technological evolution of cash money and so in theory the EU’s announcement was akin to ensuring that candles and LEDs had equal legislative prominence.

The Promise of CBDCs

CBDCs promise to combine the strengths of crypto with the benefits of electronic commerce, all with the backing of the nation-state. The goals of CBDCs are predominantly to improve the efficiency and security of domestic and international payments and settlements, enhance financial inclusiveness, enrich monetary policy tools, and combat illegal and criminal behaviour.

The digital dollar has been said to simplify and greatly speed up transactions while permanently keeping the blockchain record of all transactions. The CBDC also allows for much easier cross-border transactions which aren’t as readily available with paper Money.

Not that the motivations are necessarily pure: many posit that the enthusiasm for CBDCs by governments is a way to undermine some of the privacy that comes with using cash. Until recently, the discussion of Central Bank Digital Currency (CBDC) was generally confined to policy wonks and blockchain nerds. But recently, it has become a political issue in the US, with prospective Republican candidate Ron DeSantis promising to ban them as a threat to personal liberty. Because the federal government would have direct control over the CBDC and also a record of transactions with the digital dollar, this could be seen as both a breach of individual privacy and substantial government overreach. In the USA, where freedom is often defined as freedom from government, the digital dollar could be an extremely divisive issue and therefore, a risk not worth taking.

Why does this matter?

Fiat Currency is a very important instrument by which nations exercise their power. The risk that Fiat might lose strength to alternative means of exchange such as cryptocurrency may not seem a big deal now, but make no mistake, cryptocurrency represents more than an inchoate threat to the structure of the nation-state. Just look at the billions invested in stablecoins (privately issued crypto designed to track the valuation of a fiat currency, usually the $US), and some of the regulatory heat they have taken. All the more reason for governments to circumvent this risk and take advantage of crypto’s benefits by issuing a CBDC.

The risk for international investors is that this presents yet another layer of governmental intrusion upon privacy and trade.

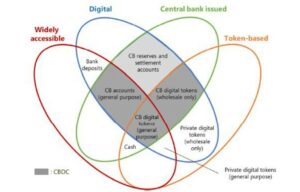

The Money Flower Source: Sampaio & Centenoe

Further, CBDCs exist on a blockchain, which cryptographically protects it and avoids the double-spend problem that has previously plagued electronic money. This is different from how funds transfers currently work, which (simply put) is an electronic representation that is underpinned by traditional fiat currency.

But, in contrast to well-known blockchains such as Bitcoin or Ethereum (which are public and permissionless), CBDCs would be issued on private blockchains. This means that the control and administration of this blockchain remain within the control of the relevant central bank/government.

That is, the details of every transaction of every dollar are permanently and immutably recorded but only the relevant government has access and control of this information. It also opens up the potential for each CBDC (which essentially would be a piece of computer code) to include within that code elements that could be activated at a later time. This potentially could give Reserve Banks and governments the power to limit the fungibility of a given dollar or even freeze or terminate it – all done remotely.

Risks for International Investors

The risk for international investors is that this presents yet another layer of governmental intrusion upon privacy and trade. Without being alarmist, CBDCs potentially create another leverage point for governments to either surveil tax or interfere in investments or business that is already legal and compliant. Given the manner in which various governments exercise their powers to limit movement during the recent COVID pandemic, it is prudent for international investors to consider this as a material risk, should CBDCs achieve widespread adoption or become the standard for inter-jurisdictional money movement.

The CBDC could also pose a huge threat to banking by sparking “bank runs”. Think about it: in volatile markets or times of financial panic, if account holders can quickly choose a CBDC as means of starring wealth, this could have a contagious effect if people decide to flock in high numbers to exchange their cash for CBDC. Or large banks with greater reserves, leverage the cost savings they make through CBDCs into higher interest rates for savings.

More broadly, a government-backed cryptocurrency could accelerate the flow of funds across different regimes, exacerbating volatility in valuations. Typically, the value of a currency has been, in the long term, based primarily on the strength of a country’s economy and their interest rates. Shifting the emphasis to CBDCs introduces risks of valuations being overly influenced by technical design features, or even different classes or ‘dollar’ depending on how the code is written.

Where does Australia stand with CBDCs?

The Reserve Bank of Australia recently concluded a pilot program into the production and use of an Aussie CBDC. The design of the project was that the CBDC was a direct liability of the RBA itself, rather than a legislated instrument. Whilst the project had many learnings. Key was the finding that for a CBDC to be made more widely available, existing regulatory frameworks would need reviewing to address some of the practical implications that arose from the use of a CBDC.

Overall, this report was very positive for the economic stimulus that a CBDC could provide the Australian economy, seeing the CBDC as a tool to strengthen and support innovation in the economy, provided legal and regulatory frameworks were adopted.

But what about privacy? In a recent speech on CBDCs in Australia, RBA Assistant Governor Brad Jones acknowledged that law enforcement would need oversight but downplayed privacy concerns based on the RBA not having an incentive to exploit user data for commercial gain. He saw that one of the main benefits of the CBDC was to increase competition and efficiency in the payments system while reducing user costs.

Cash or CBDC?

The RBA has confirmed (in Assistant Governor Jones’s speech) that while they continue to progress their CBDC research program, Australians can be confident that they will retain access to banknotes issued by the Reserve Bank for as long as they place value on them as a public good. Presumably, this is a long time.

Coming back to the EU press release, it’s interesting to observe the cultural differences in using cash that exists between Europeans and Australians. Here in Switzerland, they not only have 100 Franc notes but 200 Franc and 1,000 Franc (about $AU1720) notes as well. The EU also has 100, 200 and 500 Euro notes. In Swiss shops, it would be nothing remarkable to use a 100 or 200 Franc bill to make an everyday purchase. More expensive items are happily sold in return for the appropriate number of 1,000 Franc bills.

So, whilst it seems cash is here to stay, CBDC use continues to be increasingly explored and developed by relevant jurisdictions, risk and privacy concerns notwithstanding. Looking to the future, it is clear that CBDCs will continue to exert an influence on financial markets, albeit widespread use is still some time away. Nevertheless, it is essential that international investors understand the risks and benefits and factor this into their business decisions and portfolio designs.

Like to discuss with me how CBDCs may impact your own planning? Contact me and tell me your story!