Every international investor needs to understand the influence that exchange rates have on the return on their investments. Predicting exchange rates, especially over the short term, is notoriously difficult. This is particularly relevant for my fellow Australians living in Switzerland – how we wish this were not the case! Over the last 10 to 12 years we’ve seen the Australian dollar go from around parity with the Franc to being a very sad 58c.

Still, it’s a double-edged sword. If you are earning or investing in Francs, this could be a great time to repatriate funds down under (assuming that Australia will again be your future home).

The ebbs and flows of foreign exchange may take us by surprise from time to time. For those of us with business and life interests in more than one country it’s a good idea to have some sort of benchmark or ‘rule of thumb’ as to what represents a fair value for your home currency. I am often asked by Aussies here in Switzerland whether it is wise to repatriate funds, or invest in Francs or US dollars instead. Equally, Aussies who are looking to expand overseas, want to get an idea of when they should transfer funds over.

Whilst trying to specifically predict exchange rate movements can be a heart-breaking game, the path to getting more right than wrong starts with understanding several key factors that affect forex exchange rates:

Interest Rate Differences

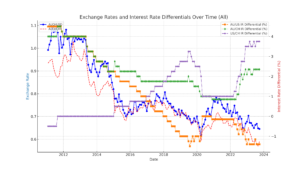

Have a look at Chart 1, which shows the Exchange Rate values and Interest Rate differentials between Australia, the US, and Switzerland (currency shown in $AU terms and interest rates as differentials between Australia and the respective country). Now, imagine you are a global currency manager back in 2011 or 2012, and you are comfortable that the risk of these three countries going broke is small enough to ignore. By holding $AU as your preferred currency, you could have got an extra 4% on your deposits.

Which currency would you buy? Back then, investors could borrow $US, exchange, and deposit it in $AU, getting an additional (almost) risk-free return on their funds. Even after this carry-trade arbitraged away the valuation difference, the additional yield was a tremendous factor in supporting the value of the Aussie.

Chart 1: AU, US and CH exchange and interest rates

Hence, a virtual circle was created for the Aussie, lifting its value up to parity and beyond with both the $US and the Franc. As soon as this interest advantage disappeared, so did the strength of the Aussie.

Economic Activity

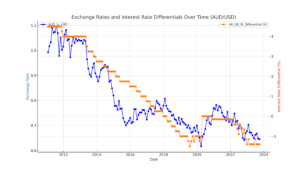

Another important factor is the level of economic activity in a jurisdiction. This drives demand for currency because if you want to invest or do business in a country, you must also pay taxes and make your purchases in that currency. Check out Chart 2, and look at what happens when Australian and US interest rates are the same, as in 2018 and 2020. Without any extra interest rate differential, the $AU is worth around $US0.72.

Why? One big reason is this is the massive differences in economies and equity markets between the two countries. There is simply more demand for $US which makes them worth more than the $AU.

Chart 2: Au and US exchange and interest rates

Deciding the best forex tactic is a question that needs to be answered within the context of your strategic financial plan.

Safe Haven Status

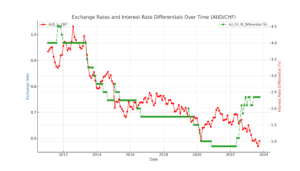

Chart 3 compares the Aussie against the Franc. Look at how the Aussie has devalued against the Franc during the time in question. Yet, during the past 13 years, the Aussie always had a net positive interest rate differential.

Australia has a population 3 times the size of Switzerland and, generally, a higher growth rate. The two countries have similar market capitalisations – so Australia more than competes with Switzerland economically.

Yet, the value of an Aussie has reduced from being above parity to about 58 centimes during this period.

Chart 3: $AU and Swiss Franc exchange and interest rates

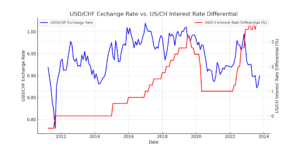

It is not just the Aussie that has been challenged by the appreciation of the Franc. Chart 4 shows the story of the $US against the Franc over the same period. Despite the strength of the US economy and the higher interest rates, the Greenback has struggled to keep at 95 centimes. Look at the two times it has fallen against the Franc recently, the first in early 2020 at COVID and a rapid decrease in interest rate differentials through doubt over the world economy (amongst other things). More recently though, despite an increasing interest rate differential, the Greenback has fallen around 10% in value.

Chart 4: $US and Swiss Franc exchange and interest rates

This trend was material enough for the US government to brand Switzerland a currency manipulator in 2020, a stance they have since rolled back. I am not sure what Switzerland was supposed to do to avoid US wrath -after all, at the time they had negative interest rates!

Both of these trends illustrate to me the influence of Switzerland’s ‘safe-haven’ status, which has supported the value of the Franc despite the headwinds of Interest Rate differentials and Switzerland’s relatively small economy. When the world is in a troubled place, the Franc is the ‘go-to’ currency, much like Gold is also seen as a safe-haven commodity.

This isn’t just anecdotal – in 2015 there was research done that concluded that in times of heightened global risk, the Swiss Franc appreciated against the Australian Dollar.

Assessing Fair Value?

Even with a good understanding of these three drivers, trying to predict exchange rate movements is a pursuit that, frankly (pardon the pun), I prefer to leave to others. There are so many factors outside of an investor’s control that you are wiser to manage your fiat exposure much as you do with other aspects of your portfolio, through diversification and hedging.

However, if you are an Australian in Switzerland, or have business interests in both countries, there are some tactical measures you can consider to take advantage of what longer-term trends can tell us. These should be done in the context of your overall financial strategy, and remember that while history may guide us, it doesn’t predict what will happen.

I find it useful to infer a rough ‘fair value’ for the three currencies, based on what they are valued at when other factors are equal. For example, when there is no interest rate differential (Chart 3, 2018 & 2020), the Aussie is worth around $USD 0.70 to 0.75. Similarly, when the US and Switzerland are on the same federal interest rate (Chart 4, 2011 – 2015), the $US ranged from 0.85 to 0.97 Francs. From this, you can make a simplistic but useful benchmark of what ‘fair value’ is for the Australian dollar.

Namely, fair value for the Aussie could be considered:

1 Australian Dollar = 0.70 – 0.75 US Dollars

1 Australian Dollar = 0.60 – 0.65 Swiss Francs

Keeping these benchmarks in mind can help act as a guide when making tactical decisions about your cash allocations and money transfers.

Navigating Choppy Waters?

For Australians currently earning income or holding investments primarily in Swiss Francs, the current valuation exchange rates could present a tactical opportunity to repatriate some of those funds back to Australia at an advantageous rate, if Australia is ultimately where you plan to settle long-term. With Swiss deposit rates hovering just above zero, parking some funds in Australian accounts earning 4%+ interest could be prudent.

On the flip side, Australians who are looking to expand their business or investments overseas may want to consider deferring any major transfers into foreign currency for now, and ideally build up foreign currency reserves slowly when the Aussie dollar eventually appreciates back closer to ‘fair value’. Focusing investments on Australian firms with significant overseas earnings in foreign currencies can also help hedge some of the currency fluctuation risks.

Also, deciding the best tactic is a question that needs to be answered within the context of your strategic financial plan, and you should be talking with your adviser before making these decisions. As always, note that this article is not specific financial advice!

Remember, although we’ve looked at a fair value for the Aussie based on the past 13 years or so, no rule says that forex values need to revert to the mean. Always diversify, so that when you need money, you have a smart place to get some from.

The most important takeaway is that foreign exchange levels often overshoot in both directions for extended periods, and sustaining valuation extremes is difficult over the long run. While the ebbs and flows of currency markets are challenging to predict, having a framework to identify when exchange rates look particularly distorted can help investors make smarter decisions on when to transfer funds internationally.

To sum up, the intricacies of currency exchange might appear enigmatic, but they conceal opportunities for the discerning investor. If you’re grappling with the complexities of how exchange rates are affecting your global assets, it’s time we talked. Let me guide you through these financial intricacies to optimise your portfolio’s performance.

References

All historic numbers in the Charts above were amalgamated from the following official sources:

FRED St Louis Reserve Bank, USA