Every one of my business clients seeks to provide a customer experience that is consistent, dependable, and reliable. These qualities are staples to produce a great experience and secure repeat business.

One reliable way to achieve this outcome is to ensure that your business has robust and detailed processes. Processes document the steps that are taken and the decisions that need to be made. These occur all along the journey from an enquiry to a sale. From one perspective, a business can be viewed as a series of processes that are designed to satisfy a customer’s needs.

Processes themselves through are constructed, like all decisions, on assumptions. But how do you manage assumptions in business decisions?

Assumptions are necessary. An assumption is a conclusion about an input that we either accept as obvious, relatively unchanging or not easy to measure.

The dangerous part about assumptions is that they can be invisible. By their very nature, we forget them.

Changing Facts, Changing Assumptions

But what happens when we get assumptions wrong? Or your conclusions change?

When looking at a person’s character, we often admire those who are constant and reliable. But let’s not get character mixed up with conclusions. John Maynard Keynes famously said:

“When the facts change, I change my mind.”

The truth in business is, you can ask yourself the same question, 6 months apart, and get a different answer. Yet both answers can be correct. Every time the facts change, we need to change our assumptions or reap the consequences.

This isn’t a sign of inconsistency. It’s a sign of evolution.

The wrong assumption, in changing circumstances, can be devastating for a business. That is because the consequences can be either material on the size or can change very quickly. Either way, it can leave your business high and dry.

Assumptions can also change in their nature. Assumptions that were inconsequential suddenly can be material.

Look at all the non-material assumptions that were made pre-pandemic, that suddenly are material.

Let’s use international air travel as an example. The material assumptions almost everyone made on a daily basis were that flights would be available at a convenient time. That there would be a competitive market between different airlines, that weather would allow travel. Pre-pandemic, these were the assumptions that really mattered.

Non-material assumptions were that borders would be open and governments would permit travel. I mean, really? When was the last time a major Western government closed their borders to travellers? Sure, you might need to apply for a visa, but unless you were headed for North Korea, you could probably get where you wanted to go.

Suddenly, with the pandemic, the non-material assumptions become VERY material. If your business depended on regular air travel – whether you were the traveller or the travellers were your customers – then you were in trouble.

Assumptions can change over time as new data appears

One of my favourite authors is Kurt Vonnegut. I was re-reading his masterpiece Slaughterhouse Five where he stated (in 1969) that the bombing of Dresden in World War 2 killed over 135,000 people. His statement was based on research by David Irving. The same David Irving that was later discredited as a Holocaust denier.

It was later uncovered that a better estimate of this tragedy was that 25,000 (I am not going to use the word ‘only’ for something of this magnitude) died.

Without taking away from the seriousness of the event, from a simple numerical perspective this is a pretty big factual error.

In an irony that Kurt may have appreciated, his figure, in a work of fiction based on inaccurate research, has become the better-known number. Simply because of the popularity of his work and the lack of a retraction in any later editions.

He assumed that Irving’s research was accurate. Yet, over time, without reviewing that assumption, dear Kurt was quite wrong.

So what has this all got to do with business?

A lot. While Slaughterhouse Five will remain in print, despite the changing data, your business can quickly be adversely affected if you make the wrong assumptions or rely on bad data. I talk more about this here in Business Decision Making for Entrepreneurs.

The solution is to regularly identify, challenge and review the assumptions you have made.

Simply being aware of the assumptions in your processes and decision-making will improve the robustness of your business.

How do you manage Assumptions in Business Decisions?

In business, if you have a problem, make it a procedure. Then you won’t have a problem any more. Depending on the size of your business, you can take a few different approaches.

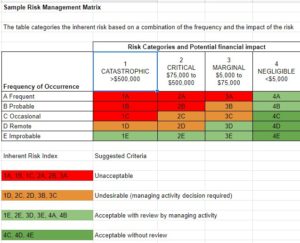

Many larger companies will adopt a Risk Management Matrix to identify and then track the assumptions – the risks – that are inherent in their business. This process has the advantage of not only identifying the risks, but working out how material they are. It includes instructions on what to do about them.

Here’s a screenshot of an example I have done, based on some of the companies I have worked with. You can download your own free copy of the Risk Management Matrix here.

Tweak this to suit your own business. Then, identify all the potential risks and assumptions you have made in your business, and assign an Index Value to them. Review this at each board or management meeting.

Your small business or start-up may not have the size to require this level of detail yet. That’s ok. Start by making a list of the assumptions and risks that are in your business, and set a diary date to review this. Make it a part of your business plan.

Simply being aware of the assumptions in your processes and decision-making will improve the robustness of your business.

Take the Creep out of Creeping

The clarity this brings is a reward in and of itself. Recently in Australia, we saw the devastating consequences of a lack of clarity in the Victorian government. They needed a whole judicial enquiry just to work out who had made the decision to hire security guards to monitor hotel quarantine. The decision-making process seems to have involved a number of people and over a short period of time, some ‘creeping assumptions’ were made.

On the Risk Management Matrix, this outcome might have been rated an ‘E – Improbable’ rating. After all, a number of senior public servants, Government Ministers and lawyers were involved.

Unfortunately for Victoria, the Risk Category was ‘1 – Catastrophic’. As a result of this creeping assumption, the hotel quarantine program was compromised and the entire state locked down for months. Thousands of people fell ill and hundreds died.

Hopefully, your business doesn’t face consequences as dire as this – but it highlights just how easy it is for assumptions to cause problems.

Role of the Business Mentor

One of the important tasks of a business mentor is to be a pair of fresh eyes into your business. A business mentor has the experience and qualifications to look afresh at your decisions. Their job is to identify and challenge your assumptions.

Gordon Livingstone tells the story of the army officer who, upon arriving in Vietnam, decries that there is a mountain where his map says there should be a valley! This had little effect on either the mountain or the reality of their situation. As Gordon said:

‘If the map doesn’t agree with the ground, the map is wrong’.

A business mentor will look at your map and compare it to the ground, and call out any conflicts. They will spot your invisible assumptions so that these can be checked and changed if needed.

Would you like to know more about how I work as a Business Mentor to help my clients achieve their goals? Contact me today – I can’t wait to hear your story!